Context

The FCA has issued a further Consultation (CP21/36) in relation to the proposed new Consumer Duty, which includes a Feedback Statement to CP 21/13. As part of the consultation, it has also published lengthy and detailed draft guidance at Appendix 2 to help firms prepare before the introduction of the new Duty. The FCA wishes to see a higher level of consumer protection in retail financial markets. It intends that the new Duty will set clearer and higher expectations for firms’ standards of care towards customers, which the FCA believes will, in turn, lead to that higher level of consumer protection.

Key points to note

The proposals for the new Consumer Duty will include:

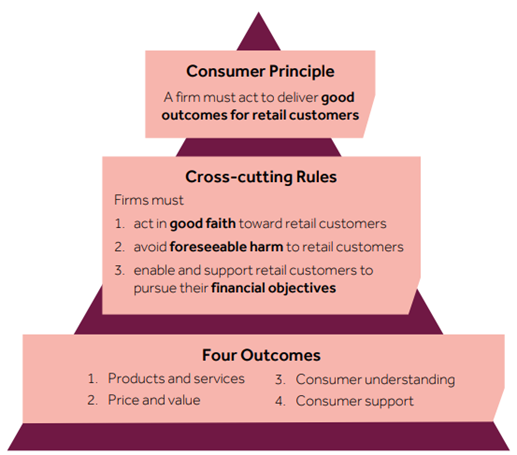

- A new consumer Principle, Principle 12 – ‘Consumer Duty’ – which will require that “a firm must act to deliver good outcomes for retail customers). This will be an objective standard that would require firms to consider the reasonable expectations of their customer base as a whole, rather than achieving the absolute best outcome for each and every customer.

- Cross-cutting rules which would set out the key behaviours required by the Consumer Duty and make clear that the Consumer Principle requires firms to:

- act in good faith

- take all reasonable steps to avoid foreseeable harm to consumers

- take all reasonable steps to enable consumers to pursue their financial objectives

These rules set out how firms should act to deliver good outcomes and therefore provide greater clarity on the expectations under the new Principle. They also help firms interpret the 4 outcomes.

- Rules and guidance relating to the 4 outcomes, which represent the key elements of the firm-customer relationship: how firms design, sell and service products and services, and the key contact points along the customer journey. They are outcomes that describe the conditions needed for consumers to be able to obtain fair value in the products and service they buy. They are:

- Products and Services: all products and services for retail customers to be fit for purpose, designed to meet consumers’ needs and targeted at those consumers. These are essential steps if firms are to act to deliver good outcomes to consumers. There is significant crossover between the proposed rules and guidance in this section and the existing Product Oversight and Governance rules.

- Price and Value: consumers to receive fair value. Again, the required outcome is very much in line with the FCA’s insurance pricing ‘fair value’ requirement.

- Consumer understanding: firms’ communications to support and enable consumers to make informed decisions about financial products and services; consumers to be given the information they need, at the right time, and presented in a way they can understand.

- Customer Support: firms to provide a level of support that meets consumers’ needs throughout their relationship with the firm. This means firms’ customer service should enable consumers to realise the benefits of the products and services they buy and ensure they are supported when they want to pursue their financial objectives.

The paper includes commentary in relation to the impact of the new Duty on existing FCA guidance in relation to vulnerability, confirmation that, at this stage, that there will be no private right of action (PROA) for breaches of the Consumer Duty, as initially discussed in the first Consultation, and monitoring consumer outcomes.

Appendix 2 of the Consultation contains lengthy (70 pages) draft non-Handbook guidance which contains useful examples of good and bad practice, behaviour that could lead to outcomes which would be likely or unlikely to satisfy the Consumer Duty.

Next actions

The consultation is open until 15 February 2022 and the FCA expects to confirm any final rules by the end of July 2022.